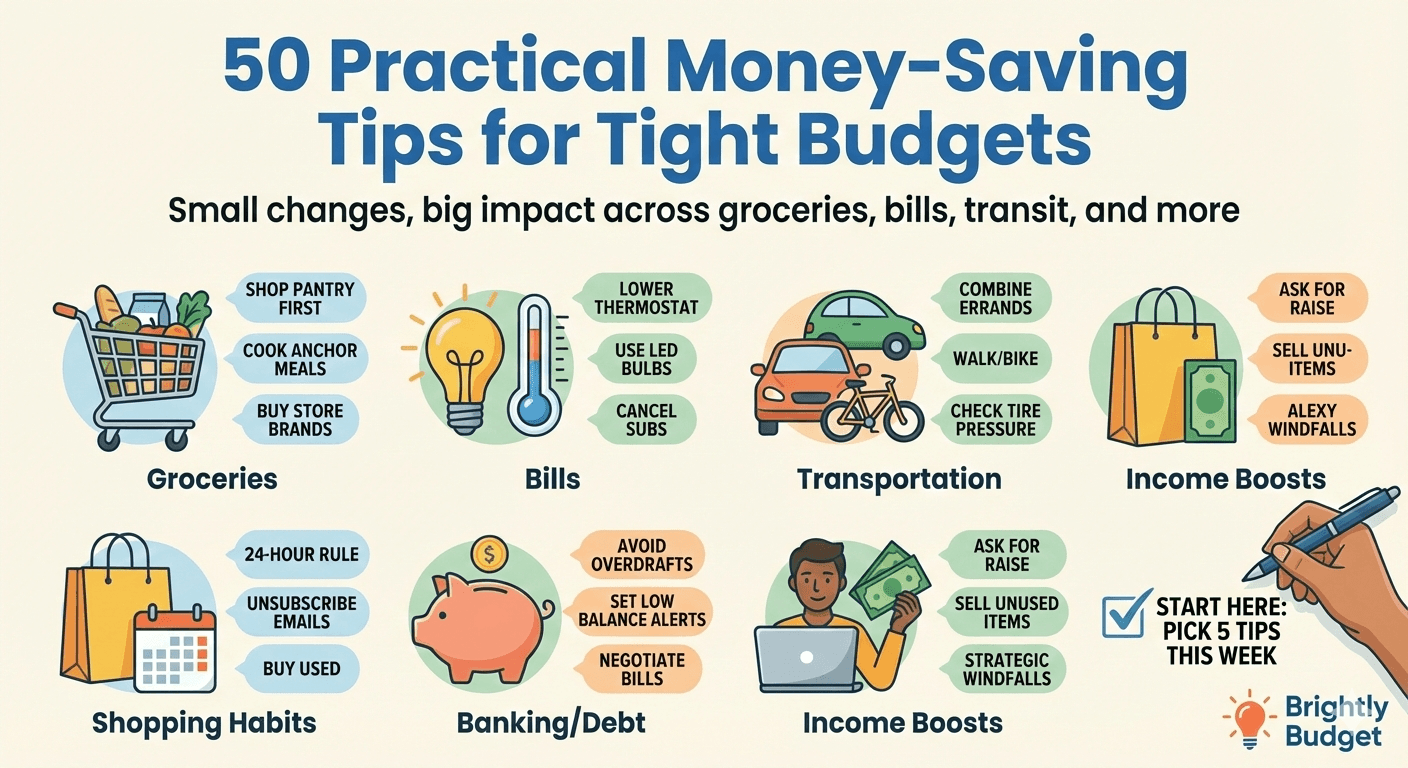

50 Practical Money-Saving Tips for Tight Budgets

When money is tight, “just cut expenses” isn’t helpful advice. You need specific moves you can actually do—without turning your life into a miserable no-fun zone.

Here are 50 practical tips you can mix and match. Pick 5 to start this week.

Groceries & food (1–12)

Plan 3–5 “anchor meals” for the week (repeat-friendly, cheap, filling).

Shop your pantry first: build meals around what you already have.

Buy store brands for basics (rice, oats, canned goods, frozen veg).

Choose cheaper proteins (eggs, beans, lentils, chicken thighs).

Keep one “emergency meal” stocked (frozen pizza, canned chili, ramen + eggs).

Use unit price (cost per ounce/gram) instead of sticker price.

Shop once per week, not “a little every day.”

Don’t shop hungry (seriously—it works).

Replace 1–2 takeout meals with “lazy dinners” (sandwiches, soup, breakfast-for-dinner).

Freeze leftovers in single portions for future busy nights.

Make water your default drink at home.

Pack lunch 2–3 days a week (start small).

Bills & utilities (13–22)

Cancel subscriptions you forgot existed.

Set a “subscription swap” rule: only one streaming service at a time.

Call your internet provider once per year and ask for a promo.

Lower your thermostat 1–2 degrees (winter) / raise it slightly (summer).

Switch to LED bulbs as old bulbs burn out.

Wash clothes cold + air dry when possible.

Avoid late fees with autopay (even minimum autopay helps).

Set phone reminders for annual bills (insurance, memberships).

Review insurance coverage yearly (shop around if appropriate).

Use a library for books, audiobooks, and sometimes streaming.

Transportation (23–29)

Combine errands into one trip (less gas, less impulse spending).

Keep tires properly inflated (fuel efficiency).

Use public transit/carpool when it’s realistic.

Walk/bike short trips when possible (bonus: free exercise).

Do basic maintenance on schedule (cheap now beats expensive later).

Keep a small “car sinking fund” for repairs.

Use fuel rewards/discount programs if you already shop there.

Shopping habits (30–40)

Use the 24-hour rule for non-essentials.

Make a “wishlist” note and revisit it weekly (most wants fade).

Remove saved cards from shopping sites (add friction).

Unsubscribe from retail emails (less temptation).

Turn off push notifications from shopping apps.

Buy used for kids’ clothes, furniture, and home goods.

Set a monthly “fun money” limit so you can spend guilt-free—inside a boundary.

Create a waiting period for big purchases (7–30 days).

Price check across 2–3 stores before buying.

Do a one-week “no-spend challenge” once per month.

Sell unused items (and use the money for a goal, not random spending).

Banking, debt, and fees (41–46)

Avoid overdrafts: keep a small buffer in checking (even $50 helps).

If you carry credit card debt, stop charging new non-essentials while paying it down.

Set alerts for low balances and large transactions.

Pay bills right after payday to avoid “accidental spending.”

Negotiate medical bills if you have them (ask about discounts/payment plans).

If you’re paying fees on a bank account, consider switching (fees add up).

Income boosts (47–50)

Ask for a raise with a concrete case (results, market range, responsibilities).

Pick one realistic side income option (short burst > burnout hustle).

Sell a service you already know (tutoring, writing, design, repairs).

Use windfalls strategically: split into debt + emergency fund + one small treat.

Start here (simple 7-day plan)

Pick:

- 2 grocery tips

- 2 subscription/bills tips

- 1 habit tip

That’s it. Small wins build momentum.

Disclosure: This post is for educational purposes and isn’t financial advice.