Budgeting 101: How to Create Your First Budget

If “budgeting” makes you picture spreadsheets, guilt, and canceling everything fun… you’re not alone.

But a budget isn’t a punishment. It’s a plan—a way to decide ahead of time what your money should do, so you’re not guessing at the end of the month.

This guide walks you through building a first budget that’s simple, realistic, and easy to maintain.

What a budget is (and what it isn’t)

A budget is:

- A set of choices about your money

- A tool to reduce stress and surprise expenses

- Something you update as life changes

A budget is not:

- A strict set of rules you “fail” if you overspend once

- A promise you’ll never buy coffee again

- A one-time project you do and forget

Step 0: Pick a “good enough” tool

Start with the tool you’ll actually open weekly:

- Notes app or paper

- Spreadsheet

- A budgeting app (especially helpful if it auto-categorizes transactions)

The best budget system is the one you’ll use consistently.

Step 1: Choose your budget timeframe

Most people start with a monthly budget (rent and bills are monthly). If you’re paid weekly or biweekly, you can still budget monthly—just do a quick check-in on payday.

Step 2: Know your monthly income

Write down take-home income (after taxes/deductions).

If your income varies:

- Use your “safe number” (your lower/typical month), or

- Use an average, but keep a buffer (ex: average minus 5–10%)

Step 3: List your “must pay” expenses

These are the bills that keep life running:

- Housing (rent/mortgage)

- Utilities

- Insurance

- Transportation basics

- Debt minimum payments

- Childcare (if applicable)

Pro tip: Don’t guess. Pull up last month’s transactions and copy real numbers.

Step 4: Estimate variable spending (the “flex” categories)

Common variable categories:

- Groceries

- Eating out

- Gas/public transit

- Shopping

- Entertainment

- Personal care

If you’re brand new, start with 10–15 categories total. Too many categories makes budgeting feel like homework.

Step 5: Add “true expenses” (the budget breakers)

True expenses are irregular—but predictable—costs like:

- Car repairs/maintenance

- Gifts and holidays

- Annual subscriptions

- Medical copays

- Travel

- Back-to-school, seasonal costs

If you don’t budget for true expenses, your budget will feel “broken” a few times per year. Instead, set up a sinking fund: a small amount each month so the bill doesn’t wreck you later.

Example: If holiday gifts cost ~$600/year, set aside $50/month.

Step 6: Pick a simple budgeting framework

Two beginner-friendly frameworks:

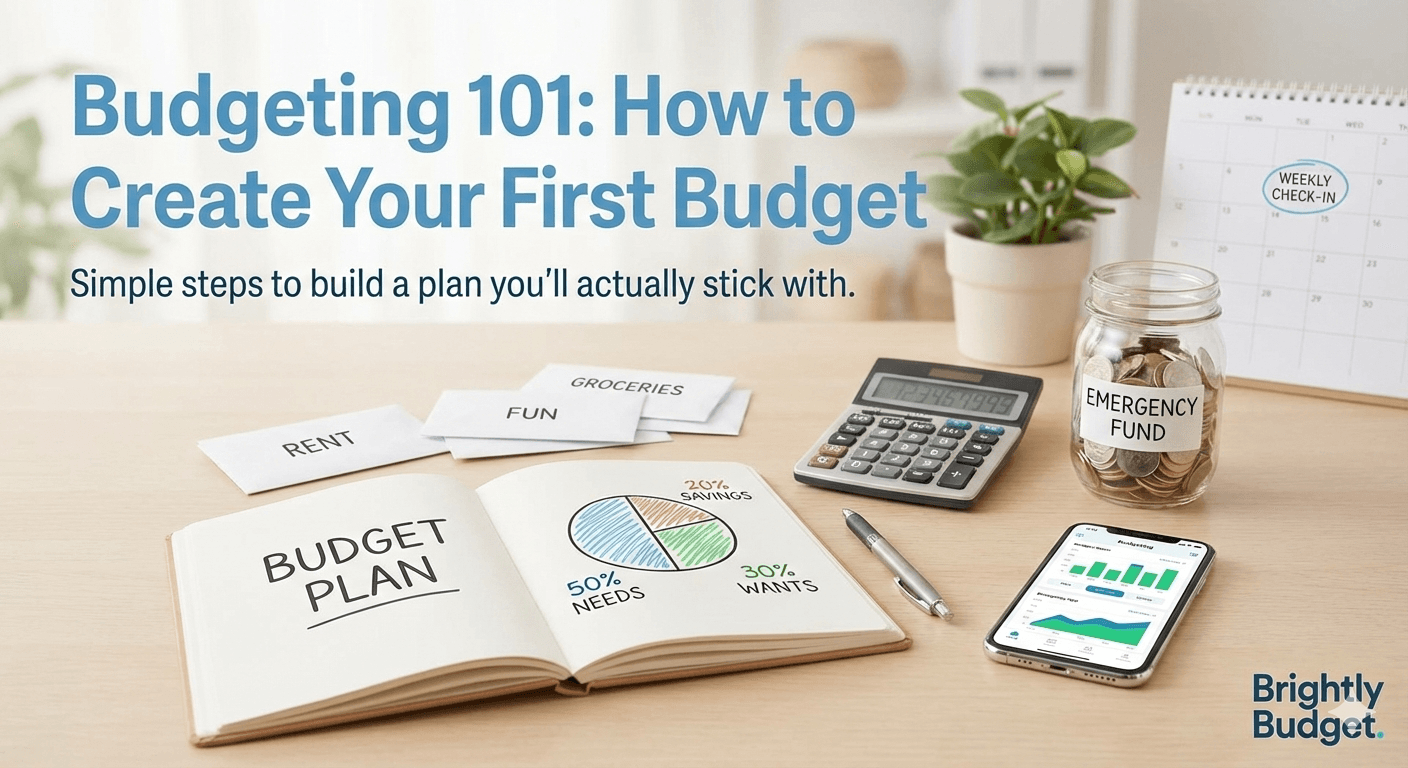

Option A: The 50/30/20 guideline

A loose guide:

- 50% Needs (housing, utilities, basic groceries, minimum debt payments)

- 30% Wants (fun, dining out, hobbies)

- 20% Savings/Debt (extra debt payoff, emergency fund, savings)

This is a guideline—not a grade. If your “needs” are currently 60% because rent is expensive, you’re not failing. You’re getting clarity.

Option B: “Every dollar has a job”

Also called zero-based budgeting. You assign all money a purpose so nothing disappears accidentally. (We’ll go deeper on this in another post.)

Step 7: Build your first draft (example)

Here’s an example with $4,000/month take-home income:

| Category | Monthly Target |

|---|---:|

| Income | $4,000 |

| Housing | $1,250 |

| Utilities + internet/phone | $250 |

| Groceries | $350 |

| Transportation | $150 |

| Insurance (monthly average) | $0 (included above / adjust as needed) |

| Needs subtotal | $2,000 |

| Eating out | $250 |

| Entertainment | $150 |

| Shopping | $200 |

| Travel sinking fund | $200 |

| Gym/hobbies | $100 |

| Fun money / misc | $300 |

| Wants subtotal | $1,200 |

| Emergency fund | $300 |

| Extra debt payoff | $300 |

| Other savings (future goals) | $200 |

| Buffer (misc/true expenses) | $0 (or add if needed) |

| Savings/Debt subtotal | $800 |

Make this yours. If “groceries” is your problem category, give it more attention and a realistic number.

Step 8: The 10-minute weekly budget habit

Budgets work when you check them regularly. Once per week:

Common beginner mistakes (so you can skip them)

- Forgetting true expenses (then feeling like budgeting “doesn’t work”)

- Being too strict (no fun money = burnout)

- Tracking too much (keep categories simple)

- Not reviewing weekly (a budget without check-ins becomes wishful thinking)

- No buffer (even $25–$50 helps)

Quick-start checklist

- [ ] Track last month’s spending

- [ ] Pick 10–15 categories

- [ ] Add a true-expense sinking fund

- [ ] Set 10-minute weekly review on your calendar

- [ ] Keep a small “fun money” category so the budget is livable

Disclosure: This post is for educational purposes and isn’t financial advice.

Put these ideas into practice.

Download Brightly on iOS or Android and manage your money — or create an account on the web today.

New to Brightly? Create an account·Subscriptions available in the app only